Climate Goal for 2040: A New Milestone for the EU

On 6 February 2024, the European Commission (EC) published a detailed impact assessment on possible pathways to reach the agreed goal of making the European Union climate neutral by 2050. Set against this backdrop, our VITO/EnergyVille colleague Wouter Nijs and Advisor to EnergyVille Ronnie Belmans joined forces to provide us with insights into the EC’s resulting recommendation of a 90% net greenhouse gas emissions reduction by 2040 compared to 1990 levels. As such, this insightful article aspires to serve as a quick source of information for stakeholders and policy makers alike – tackling emission reduction, energy efficiency, electrification, innovative fuels and land use.

Purpose of the publication

The European Commission’s Impact Assessment Report evaluates various levels of EU greenhouse gas emissions in 2040. It discusses potential climate goals for 2040, aligning with the EU’s aim to be climate-neutral by 2050 as required under the European Climate Law. The evaluation includes the greenhouse gas budget (total emissions over the full period of CO2 and other greenhouse gases) and feasibility, including costs and technological implementation. Unfortunately, at the time of writing, only figures for the EU are available – not for individual member states.

Any changes to the EU’s 2030 climate goal?

No, there are no changes to the EU’s climate goal for 2030, which still aims to reduce net greenhouse gas emissions by at least 55%.

Current legislation is estimated to result in a 57% reduction in greenhouse gas emissions by 2030 compared to 1990. Significant reductions are still needed when it to comes to buildings and transport, where decarbonization has been slow – in the case of transport – even moving in the opposite direction. The success of the ‘Fit-for-55’ legislation depends on implementation – including the ongoing process of updating National Energy and Climate Plans (NECPs), for which Member States are due to submit their next NECP to the European Commission in June this year. The Green Deal Industrial Plan – with its key pillars Critical Raw Materials and the Net Zero Industry Act – plays an essential role in achieving sustainable industrial transformation. There is, however, less reporting on hydrogen in the path to 2030 than before, with the EU only reporting mandatory green hydrogen linked to all RFNBO targets (Renewable Fuels of NonBiological Origin), such as greening 42% of industrial hydrogen.

Preferred option: 90-95% reduction by 2040

For this article, we relied upon the preferred trajectory as a basis, achieving an emission reduction of 92% by 2040 compared to 1990 – a reduction which aligns with the recommendation of the European Scientific Advisory Board on Climate Change (ESABCC). This option represents the most efficient route to climate neutrality in 2050, with the highest net benefits in terms of avoided climate impact and air pollution, and only slight cost increases compared to other less ambitious trajectories. For the period after 2030 (2031-2050), the average annual cost for the energy system transition is €20 billion higher compared to the ‘middle’ option, which is an extension of current policies and reduces greenhouse gas emissions by 88%. The benefits of avoided climate change and air pollution are greater, estimated at €23 to €43 billion annually.

Is this a surprise?

Yes and no. There has been a long-standing aim for a faster reduction between 2030 and 2040 than between 2040 and 2050. In 2020, there was already talk of an 85% reduction by 2040, which received little attention as the focus back then was on legislation for 2030 and 2050. Without adjustment to EU policy, the reduction is already 88% in 2040. What is particularly new now, however, is the details of what exactly is needed for this.

Which sectors mainly reduce greenhouse gases?

A reduction of 92% in greenhouse gases by 2040 compared to 1990 corresponds to 90% compared to 2015. This indicates that remaining emissions are very small, requiring significant contributions from all sectors. Simplified, relying on the preferred trajectory as a basis, in 2040, the energy sector will emit virtually nothing (electricity and heat generation, fuel production, etc.), while emissions from energy use in industry, buildings and transport will each decrease by about 85% compared to 2015.

Energy efficiency first

With that same preferred trajectory as a basis, in 2040, total energy use in the EU decreases by about 30%, from around 17 000 TWh in 2021 (61 EJ) to about 12 000 TWh (43 EJ), and this mainly due to the electrification of vehicles and heating in buildings and industry. This change does, however, require significant investments – most noteworthy a doubling of yearly investments in private buildings, from an average of €116 billion in 2011-2020 to €248 billion in 2030-2040.

Financial feasibility varies greatly depending on household, income level and the type of renovation, but robust financial support is in any case essential for affordable renovations. Furthermore, the success of renovation investments depends not only on financial support, but also on awareness, knowledge of renovation options, the availability of qualified personnel and trust in contractors.

Extensive electrification and the rise of innovative fuels

The preferred trajectory indicates that electricity becomes the main energy carrier, with a share in final energy use of over 45% in 2040. Indeed, electricity production grows from about 2900 TWh in 2021 to 5200 TWh in 2040. This is a significant challenge, because – since 2003, for 20 years –

electricity production has fluctuated between 2800 and 3000 TWh. The share of renewable energy in total electricity generation rises from about 40% in 2021 to 87% in 2040, with wind and solar energy having the largest capacity. Electricity production from renewable sources grows by a factor of almost four, reaching 2.3 TW of renewable capacity in 2040. Flexible solutions, storage and electrolysis play a key role. Installed nuclear energy capacity decreases slightly, from 94 GW in 2030 to 88 GW in 2040 in line with the recently announced nuclear policy (71 GW in the standard scenario).

At the same time, the use of non-biological renewable fuels such as hydrogen and electrofuels becomes more important. Hydrogen production reaches levels of 30-35 Mton, of which about half is used to produce these electrofuels. Hydrogen can be produced with renewable electricity. In 2040, about 1500 TWh of electricity would be needed to produce hydrogen and electrofuels. Electrofuels can be made with electricity and captured carbon dioxide or carbon monoxide, with or without hydrogen. It is also possible to combine nitrogen with hydrogen, resulting in ammonia as a fuel. This, however, is not mentioned in the EC’s impact assessment. In 2040, these innovative fuels would account for 20% of energy use in the transport sector, especially shipping and aviation. In buildings, these fuels would be almost unused.

70% less fossil fuel use

The use of renewable energy in the energy mix grows as the use of fossil fuels diminishes. Indeed, fossil fuel use decreases by more than 70% by 2040, while renewable energy rises. Import dependency drops from 61% in 2019 to 26% in 2040. However, the high demand for renewable energy, storage and new technologies can lead to new dependencies on raw materials or technology imports from non-EU countries. For batteries for electric vehicles, 80 000 tons of lithium per year would be needed in 2040. As a comparison, global lithium mining in 2030 is estimated at 721 000 tons. It is, however, worth noting that this becomes less critical over time: if such materials are imported, they are recyclable with high efficiency rates and this multiple times over, unlike fossil fuels.

Second-generation energy crops

Bioenergy increases, driven by advanced liquid biofuels and biomethane. The higher demand for biomass is partly met by an increase in lignocellulosic crops such as Miscanthus (Elephant Grass) and Switchgrass. These can be used to produce second-generation biofuels. About 11 million hectares would be needed in 2040 (6% of the current EU agricultural area). However, the overall increase in agricultural area is only 1 million hectares because there is a sharp decrease in crops for first-generation biofuels. Forest areas increase by about 5 million hectares, and about 1.5 million hectares of grassland are converted into peatland that efficiently store carbon.

All hands on deck for land use, forestry and negative emissions

The largest contribution to the reduction comes from standard emission reductions – achieving a decrease of about 3000 MtCO2-eq in greenhouse gases, equivalent to an 81% reduction. With the addition of conventional CCS (Carbon Capture and Storage), a reduction of 84% is achieved. However, negative emissions are essential for the intended net reduction of 92%. Natural CO2 uptake, as well as technologies like CCS (Carbon Capture and Storage), BECCS (Bio-Energy with Carbon Capture and Storage), and DAC (Direct Air Capture), play a crucial role in CO2 reduction.

The various components of the emission reduction from 2015 (3914 MtCO2-eq, excluding LULUCF) are as follows:

- 2,997 MtCO2-eq: standard emission reduction

- 169 MtCO2: annual capture and permanent storage (CCS) of process emissions or fossil-origin CO2

- 317 MtCO2-eq: annual natural negative emission in the LULUCF sector (Land-Use, Land Use Change, and Forestry: such as tree growth and carbon sequestration in the soil). This sector had a negative contribution of -322 MtCO2-eq in 2015, but this contribution has become much smaller in recent years, which the EU aims to restore.

- 75 MtCO2: annual negative emission, carbon capture and storage via DACCS (Direct Air Carbon Capture and Storage) and BECCS (Bio-Energy with Carbon Capture and Storage).

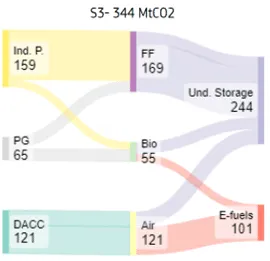

The use of industrial carbon removal would be 75 MtCO2 by 2040 – almost 22% of the total carbon capture. Additionally, about 100 MtCO2 would be captured mainly from the air (DAC) and used for the production of e-fuels (CCUS). (See Figure 1)

Figure 1: Flows of captured CO2 in 2040 Note: “Ind. P.” stands for Industrial Processes and includes fossil carbon from industrial processes as well as carbon of biogenic origin coming from the upgrade of biogas to biomethane. “FF” stands for “Fossil Fuels”. “PG” stands for “Power Generation”. “Bio” refers to CO2 produced by the combustion of biomass in power generation and produced during the upgrade of biogas into biomethane. “DACC” stands for “Direct Air Capture of CO2”, for underground storage (DACCS) or use in e-fuels. Source: PRIMES