Recently, the VITO/EnergyVille research team of the Smart Energy & Built Environment Unit put pen to paper for its latest publication ”Winter is Coming. Where are the Heat Pumps?”—a position paper that brings together their substantial research efforts regarding the support of policies and the implementation of projects involving heat pumps.

As winter is coming, and heating our homes is top of mind, in this Expert Talk, we are happy to walk you through the position paper’s key takeaways.

Both the position paper and this accompanying Expert Talk came about thanks to the input of multiple EnergyVille colleagues, but wouldn’t have been possible without the contribution of its main VITO/EnergyVille authors Christina Protopapadaki, Maarten De Groote and Birgit Vandevelde.

Backdrop

There is no beating about the bush in the latest report by the United Nations’ Intergovernmental Panel on Climate Change (IPCC): in the face of the escalating challenges posed by climate change, the imperative to forge a path towards cost-effective decarbonization has never been more pressing [1]. Hand in hand with the need for urgent and impactful measures, go strategic choices that consider an integrated societal approach. And in that regard, an up-close look at the heating of our building stock is indispensable—both in terms of the role different technologies can and should play, and in terms of the balancing act between demand reduction and decarbonising our heat supply.

In the autumn of 2022, EnergyVille launched PATHS2050 — The Power of Perspective, an online platform which offers key insights into achieving a cost-effective decarbonization of Belgium across an array of different sectors. And, when looking at the results of the currently explored scenarios for the building stock, we see they all consistently point in the direction of a common outcome, regardless of the scenario considered: combined with demand reduction, a massive deployment of heat pumps is needed, complemented by district heating1.

The combination of the above thus incentivised the VITO/EnergyVille research team of the Smart Energy & Built Environment Unit to put pen to paper in a position paper, summarising their own substantial research efforts regarding the support of policies and the implementation of projects involving heat pumps.

As winter is coming, and heating our homes is top of mind, in this Expert Talk, we are happy to walk you through the position paper’s key takeaways.

The rise of the heat pump

Heat pumps are a mature technology that, in recent years, has consistently been improved to allow for versatile individual and collective applications in the residential sector. Meanwhile, given that they are very efficient in delivering heat, they are considered to be of paramount importance to decarbonise building stock heating. As a result—within the framework of the EU’s commitment to rapidly reduce dependence on (Russian) fossil fuels and fast forward the green transition2—we see that building related policies at both Member State and EU level, coupled with the energy crisis and heightened awareness of the energy transition, have recently moved heat pumps to the forefront of the energy transition.

On a Member State level, heat pump rollout is being facilitated throughout Europe with policies such as bans on gas connections to the grid for new homes in the Netherlands and Flanders3, mandatory shares of renewable energy in heating systems in Germany4, and greenhouse gas emission limits to new heating systems in France5.

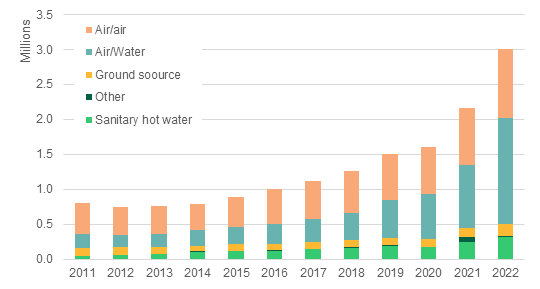

Belgium, for example, has recently witnessed a rapid acceleration in the rollout of heat pumps—albeit one which currently seems to be prominently confined to new constructions, with the transition still gaining traction in existing buildings. This acceleration can be attributed to a potent cocktail consisting of the energy crisis, an increased awareness of the energy transition, and newly introduced building related policies. In Flanders specifically, the “Warmteplan 2025” (Heat Plan 2025) foresees financial support for the installation of heat pumps, as well as the phasing out of oil boilers and the banning of gas connections in new buildings [2]. Because of all of these factors, sales of heat pumps and heat pump boilers saw an increase of no less than 140% in the first half of 2023 compared to the previous year, with heat pumps representing a quarter of all heating system sales6. Thus, while it remains of utmost importance to acknowledge that the uptake in existing buildings is still running at too slow a pace, this rapid acceleration in new constructions is hard to miss. And the same accelerating trend is noticeable on a European level, where sales data from 16 European countries show a 38% increase in heat pump sales in 2022, outpacing the 34% rise in annual sales of 2021 [3], [4].

Figure 1: European heat pump sales development by type (“Air/air counts heat pumps with a primary heating function). Source: Adapted from EHPA [4]

At the same time, on an EU level, the European Commission recently initiated a call for evidence and public consultation to establish a dedicated Heat Pump Action Plan7—an initiative that aims to further accelerate the heat pump deployment in Europe by focusing on legislation, financing, communication and skill building, as well as by setting up a Heat Pump Accelerator platform that will bring all relevant stakeholders together. With this plan, the European Commission’s objective is to install at least 10 million additional heat pumps by 2027.

Bumps in the road

While the public consultation for the Heat Pump Action Plan has consolidated the common understanding that heat pumps will play a significant role in achieving the climate and energy goals of the European Union, it has equally highlighted the fact that substantial effort will be required to sufficiently accelerate the deployment of heat pumps.

Ideed, the bumps in the road are currently still manifold. Grid readiness, building readiness, lower upfront and n operational costs, affordability and skilled workers are but some of the main aspects requiring our immediate attention, as identified in the public consultation. At the same time, the lack of reliable and easily accessible information, among others, can be an important factor hampering acceptance of the technology.

The need for a compass

In short, more evidence as well as clearer communication are needed to both strengthen policies and promote acceptance and market uptake. All stakeholders across Europe—including policymakers and citizens—could benefit from a compass in the shape and form of more transparent and trustworthy information on which to base their decisions:

Under which circumstances does the installation of heat pumps make sense—from a technical, economic and broader societal point of view? Which buildings should be prioritized to adopt heat pumps? What is the role of energy efficient renovation? Which policies are required to expediate deployment, while at the same time ensuring that the necessary complementary measures—such as energy efficiency improvements—are concurrently addressed?

A thorough and fact-based analysis can assist in comprehending crucial issues and identifying possible measures to mitigate them.

Let us then turn to the findings of our research8, addressing five pivotal elements that influence the viability of heat pump deployment in residential buildings, offering evidence-based insights into each.

Five pivotal elements

1. Favourable market conditions for heat pump rollout in existing buildings

First of all, initial investment cost is a crucial deciding factor prompting—or not prompting—people to purchase a heat pump, and it depends on three main elements: the capacity of the heat pump, the type of heat source and the cost of installation. Regarding the latter labour cost of installation, we notice this varies significantly from country to country—making for the fact that that is where lies the largest potential for lowering the initial investment cost.

Furthermore crucial is whether the existing heat distribution system suffices for proper operation or not. Here, we see that often indeed it does suffice, as in many cases the system is overdimensioned due to prior renovation works or initial oversizing.

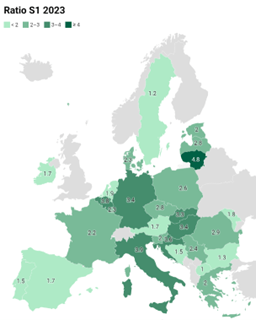

Another particularly influential factor for the rollout of heat pumps is the relationship between electricity and fossil fuel prices. This price ratio varies significantly—both over time and from country to country, as it is highly dependent on the geopolitical context and policies. Figure 2 shows how the ratio significantly differs between European countries.

Figure 2: Visualisation of electricity to gas price ratio for household consumers in S1 of 2023. Own visualisation based on Eurostat.

Table 1 below shows us the percentage of heat delivered by the heat pump part of a hybrid system for different price ratios. Thus, we see that for a price ratio of 4.5—on average in line with prices in Flanders between 2015 and now—it is not interesting, in terms of operational costs, for buildings with any insulation level to operate a heat pump or run a hybrid system in heat pump mode. Contrarily, at a ratio of 1.8, the preferred operation of the heat pump over the gas boiler for most of the time is self-evident, even for poorly insulated homes. Thus, in general, the tipping point for the profitability of operating a modern heat pump in the Belgian context occurs at electricity/gas price ratios below 2.5.

Table 1: Influence of electricity/gas retail price ratio on the decision matrix for medium-sized terraced buildings, with oversizing factor of 1.3 and 18°C indoor temperature setting. The decision matrix shows the proportion of heat supplied by the heat pump in a year for different insulation levels, as explained in footnote 99.

2. Technical feasibility

The technical feasibility of heat pumps is well-established, as they operate on the principles of thermodynamics and have been proven effective for both heating and cooling applications. Advances in technology have led to the development of highly efficient and reliable heat pump systems, making them a technically viable and sustainable option for residential, commercial, and industrial heating and cooling needs.

The possibility of installing a fully electric heat pump is mainly determined by the energy performance of the building and the design temperature regime of the delivery system. Indeed, the combination of these two parameters is crucial to determine the feasibility of different system designs. Understanding in which cases the design load is remarkably high, or the operating conditions are suboptimal—as they are in conditions requiring too high supply temperatures—can help avoid unnecessarily expensive applications of heat pump technology.

Although heat pumps are technically feasible in most dwellings, the required heat pump capacities are not always available. Therefore, an improved energy performance can help reduce the heating demand—limiting the required size. Depending on the current state of the building, moderate interventions such as replacing the windows or the roof insulation can, in many cases, be sufficient from a technical point of view. However, for the least performing dwellings, deeper renovations can additionally improve the lifecycle cost.

On the other hand, lowering the supply temperature of the hydronic heating system can also allow for a low-temperature system, thus decreasing the cost of the heat pump. This upgrade of the emission system can be achieved through booster technology or simply with additional emission elements. Where these solutions are not sufficient, high-temperature heat pumps are available—albeit at a higher cost.

For buildings with very high thermal needs, hybrid systems that combine a heat pump and gas boiler are another option. Although it does have to be noted that while they help improve energy efficiency without the need for renovation, in the future they may still have to be replaced by fully electric heat pumps—depending on the long-term policies applied in each country.

3. Contribution of a PV system

Heat pumps require a substantial amount of electricity to operate, which often leads to the suggestion of installing solar photovoltaic (PV) panels to cover the heat pump electricity consumption. The context of energy market reform has, however, turned the economic sense of combining heat pumps with PV panels into a somewhat more subtle question.

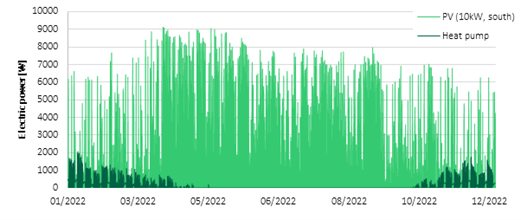

With low feed-in tariffs and a shift to capacity-based network charges, it is important to maximise self-consumption of this combination of technologies. Figure 3 shows the yearly heat pump electricity demand profile for a typical well-insulated Flemish house in dark green, overlayed with the electricity generation of a large south-oriented PV system in light green.

Figure 3: Yearly heat pump electricity demand profile for a typical well-insulated Flemish large, terraced house with high thermal insulation (dark green) and local PV production (10 kWp installation, south oriented) (light green).

We note the self-consumption is low—due to both a seasonal and time-of-day mismatch of the heating demand and the PV generation. Indeed, the typical thermostat settings for a working family require heating when the sun is not yet up, or already down. This makes for the fact that an average load cover factor (proportion of load covered by the PV) of just under 10% was found for typical heating profiles.

Of course, by using intelligent control systems that respond to the thermal buffer capacity of buildings, the electricity demand can be shifted by a few hours in well-insulated buildings in order to improve the match with local PV production. However, even in this case, the coverage of heat demand by PV is still limited to approximately 15 to 20% [5], [6].

Electric storage, then, could offer a partial solution to increase self-consumption on a daily basis and allow for a better integration of renewable energy technologies. However, given the large seasonal mismatch between heating demand and PV generation, a more efficient approach would be to optimise self-consumption at the level of building clusters, rather than individual dwellings. This way, one could make use of different demand profiles—including non-residential loads—which, combined, could follow the potentially available local renewable electricity production more closely.

4. Role of the heat pump in cost-optimal renovation

The latest proposal for a revision of the Energy Performance of Buildings Directive (EPBD)10 foresees Minimum Energy Performance Standards (MEPS) to ensure a higher renovation rate of existing buildings—thus aiming to achieve a fully decarbonised building stock by 2050. Assessment of the cost-optimality and cost-effectiveness of these MEPS allows for a comparison between different renovation measures—making it interesting to see how heat pumps compare to condensing gas boilers.

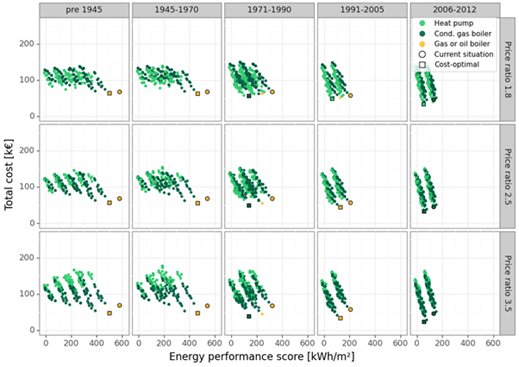

In the cost-optimal renovation analysis of 135 reference buildings, achievable energy performance scores were plotted against the total lifecycle cost. For each renovation package, the original heating system was highlighted, comparing the packages with a heat pump and with a condensing gas boiler. This was done for three price scenarios, and both the theoretical EPC-calculated energy use and the adjusted “real” use respectively.

Running calculations for the theoretical EPC energy use showed that the total lifecycle cost for the heat pumps decreases for the lower energy price ratios and is about the same as for gas boiler solutions for a ratio around 2.5. In this case, heat pumps are part of the cost-optimal solutions.

As shown in Figure 4, the picture is quite different when looking at the estimated “real” consumption, where the total cost of the current state is always lower than that of solutions with a heat pump, especially for badly insulated buildings. This is so because the “real” current consumption is much lower than the theoretical EPC-calculated consumption for low energy performance levels. The differences in “real” use and EPC-calculated use are a result of two effects. The prebound effect, under which occupants of badly performing buildings reduce their energy use below standard comfort levels to save money. And the rebound effect, under which occupants consume more energy after renovation to improve their comfort compared to before. Within this context, it is worth noting that while the cost savings may be more limited than expected, the comfort gains and value increase can be significant.

When improving the building’s performance towards 100 or even 200 kWh/m2, however, heat pumps do become the most cost-effective system for the lower energy price ratios.

Thus, the above allows us to conclude that while lower price ratios are vital, deciding factors beyond purely financial considerations—such as regulation and comfort, or value increase—are equally needed to justify the viability of heat pumps.

Figure 4: Mapping of the cost and performance of different renovation packages for semi-detached dwellings of average size and insulation quality and five construction periods (columns). The rows compare different price ratio scenarios. The resulting total cost is based on energy demand calculated with the EPC methodology, but the demand is corrected to represent real consumption.11

5. Grid impact

Heat pumps can assist the grid if smart control is used, and the system is designed for both efficiency and flexibility [7].

However, when such smart control is not in place, heat pumps—just like other large loads, such as electric vehicle charging—may create congestion and power quality problems in the local grid. Thus, cumulatively, in the electricity system of a region or country, they may lead to increased demand for electricity production and distribution capacity.

In general, neighbourhoods with larger uninsulated buildings will have larger issues if all buildings are equipped with a heat pump, because of the generally higher required capacities. However, the simultaneity11 of the loads also plays an important role. And, as there is a large dependence on the outdoor temperature, high simultaneity is to be expected between heat demand of buildings in the same neighbourhood, region or country. Indeed, for fully electric heat pumps, the simultaneity can be as high as 75% in a small rural neighbourhood connected to one distribution feeder, considering Belgian residential buildings [8]. This simultaneity of loads diminishes, however, as the number of loads increases.

Thus, it is important when proposing decarbonisation policies focused on the electrification of heating, to consider the potential impacts on the security of supply and grid stability. Something which equally entails that grid operators need to stay up-to-date and foresee scenarios that reflect ambitious policies for heating electrification, even more so in the face of the parallel electrification of mobility.

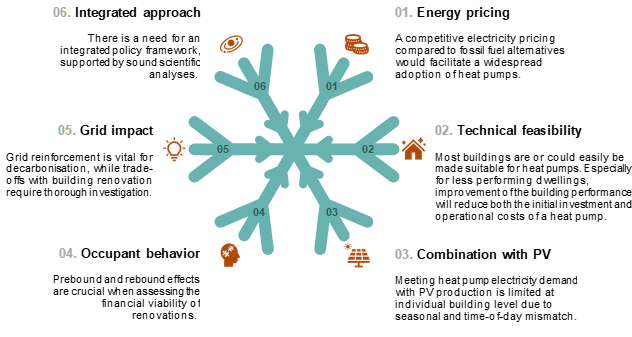

Six key recommendations

Heat pumps are at the forefront of the energy transition in Europe. And unsurprisingly so, given their potential towards decarbonisation, their highly efficient performance and their versatile applications. The European Commission’s upcoming Heat Pump Action Plan initiative is set to accelerate their deployment, and so are various policies already undertaken in several European Member States.

Despite that, more fact-based information concerning the technology, its benefits and its applications are needed to support both policymaking and implementation on the ground. Thus, on the basis of the research findings which lay the foundation for this Expert Talk, we would like to conclude by proposing the following six key recommendations to accelerate the roll out of heat pumps in residential buildings.

Figure 5: Recommendations to expedite the deployment of heat pumps in residential buildings

1. A competitive electricity pricing compared to fossil fuel alternatives would facilitate a widespread adoption of heat pumps.

While the higher initial investment cost of heat pumps compared to gas boilers is a significant factor to consider, their increased efficiency does allow for a potential offset against this difference in initial investment cost. All the more so because our research indicates that competitive electricity pricing, in comparison to fossil fuel alternatives such as natural gas, enhances the economic viability of heat pumps for homeowners. Indeed, in a climate and building stock similar to that of Flanders, a required electricity-to-gas price ratio of 2.5 or lower would render heat pumps economically competitive against gas boilers.

That being said, any energy taxation reform should be complemented by an approach tailored to vulnerable households, so as to ensure a just transition for all.

2. Most buildings are or could easily be made suitable for heat pumps. Especially for less performing dwellings, improvement of the building performance will reduce both the initial investment and operational costs of a heat pump.

From a technical point of view, most buildings are already suitable for heat pumps, or could easily be made to be so after some simple adaptations or limited renovation.

The possibility of installing a fully electric heat pump is mainly determined by the energy performance of the building and the temperature regime of the heat delivery system. Lowering the supply temperature of the hydronic heating system can allow for a low-temperature system, thus decreasing the cost of the heat pump. This upgrade of the emission system can be achieved through booster technology or simply with additional emission elements. Where these solutions are not sufficient, high-temperature heat pumps are available—albeit at a higher cost.

3. Meeting heat pump electricity demand with PV production is limited at individual building level due to seasonal and time-of-day mismatch.

Analysis of a PV production profile and a heat pump electricity demand profile shows that there is both a seasonal and a time-of-day mismatch for a Belgium-like climate and latitude, where PV production can only cover the heat pump load for space heating for around 10%.To improve the absorption of local renewable energy production, optimisation at the level of multiple buildings—whereby the variable needs of different users can be combined—would be more beneficial than optimisation at an individual building level.

In warmer climates with significant cooling needs, heat pumps can be a good combination with PV, as more coincidence of the demand and production can be expected.

4. Prebound and rebound effects are crucial when assessing the financial viability of renovations.

When examining the total cost over a period of 30 years, the outcomes depend significantly on the energy price assumptions, with the retail electricity-to-gas price ratio needing to drop below 2.5 for heat pumps to topple condensing gas boilers and become part of the cost-optimal renovation packages.

However, real energy use—especially in buildings with limited or no insulation—has been shown to be much lower than the one estimated by the energy performance calculation method based on asset rating.

For policy makers and building owners to be able to make better informed decisions, more knowledge and evidence is required about the patterns of energy use before and after renovation, as well as about the co-benefits that energy renovation offers.

5. VGrid reinforcement is vital for decarbonisation, while trade-offs with building renovation require thorough investigation.

While conducting a detailed assessment of the impact of heat pumps on the electricity grid proves challenging, it is feasible to estimate the evolving total number of heat pumps and the anticipated peak demand for a country or region.

In the context of Flanders, projections suggest an installation of 0.35 million to 2.4 million heat pumps by 2035—subject to market conditions and policy ambitions. Currently, grid adequacy studies in Belgium do not encompass more ambitious scenarios, despite the imperative of meeting European and national climate targets.

Acknowledging that investments in thermal insulation can diminish peak demand by reducing required heat pump capacity, a trade-off emerges between renovation spending and investment in grid reinforcement and generation capacity. Investigating this trade-off at a localized level—considering neighbourhood-specific needs—is essential to be able to devise tailored transition pathways.

6. There is a need for an integrated policy framework, supported by sound scientific analyses.

While heat pumps may be technically feasible for many buildings in Flanders and Europe, the uptake of the technology in existing buildings remains slow.

Energy policy for the decarbonisation of the building stock requires a broadly integrated framework that unifies technological, economic, social and context-related factors. An optimal package of combined polices and regulations to bolster the roll-out of heat pumps should be context-specific and potentially combine both global measures such as energy taxation reform, and local measures such as investment support. Along with assistance for vulnerable households, a balanced policy package would also reduce the need to subsidise those that are able to invest.

Footnotes

- EnergyVille Paths 2050: https://perspective2050.energyville.be/residential-commercial

- REPowerEU: https://neighbourhood-enlargement.ec.europa.eu/news/repowereu-plan-rapi…

- The Netherlands has banned the connection to a gas grid for new-build homes since 2018. https://www.iea.org/policies/12207-gas-act-no-mandatory-connection-of-n… There is also a general ban on gas connections for new-builds in Flanders from 2025. https://www.vlaanderen.be/nieuwe-verwarmingsinstallatie-kiezen/geen-aar…

- Germany planned to effectively ban new gas boilers from 2024 by requiring new heating appliances to operate with at least 65% renewable energy, limiting options to heat pumps, biomass and district heating. After strong opposition, this ban was eventually linked to municipal heat plans and thus delayed until 2026 for large cities and 2028 for smaller cities. Source: https://www.cleanenergywire.org/factsheets/qa-germany-debates-phaseout-…

- In Frankrijk schrijft een decreet uit 2022 voor dat het niveau van broeikasgasemissies van nieuwe verwarmingsapparatuur of apparatuur voor de productie van sanitair warm water lager moet zijn dan 300 gCO2eq / kWh NCV. Dit betekent de facto het einde van nieuwe kolen- en stookoliegestookte verwarmingstoestellen in woongebouwen. https://climate-laws.org/document/decree-no-2022-8-relating-to-the-mini…

- (in Dutch) https://www.infowarmtepomp.be/nl/nieuws/verkoop-warmtepompen-stijgt-met…

- European Commission, Heat Pump Action Plan Initiative: https://ec.europa.eu/info/law/better-regulation/have-your-say/initiativ…

- While the studies underlying this position paper are mostly related to the Flemish building stock and context, it is important to realise that valuable insights can be drawn for other European countries that share similar challenges —either technical, regulatory or market-related. Furthermore, the methods and models used to derive these results can be easily altered to analyse other contexts.

- Each number in the decision matrix shows the proportion of heat supplied by the heat pump of the hybrid system in a year, which is based on the economically best option in each time step. The building envelope insulation level in the rows indicates the situation before renovation, while the insulation level in the columns indicates the situation after renovation. Therefore, the diagonal gives the buildings in their original state. Moving horizontally to the left one finds the result for the same building after renovation to a higher insulation level.

- https://energy.ec.europa.eu/topics/energy-efficiency/energy-efficient-b…;

- Simultaneity factor of 0.6 or 60%, for example, indicates that the simultaneous peak of all loads is 60% of the theoretical peak where all loads have their peak at the same time.

References

[1] IPCC et al., ‘AR6 Synthesis Report: Climate Change 2023’, Jul. 2023. doi: 10.59327/IPCC/AR6-9789291691647.

[2] De Vlaamse Minister Van Justitie Handhaving Energie En Toerisme, ‘BIS-VISIENOTA AAN DE VLAAMSE REGERING - Visienota Warmteplan 2025’, 2021. Accessed: Nov. 16, 2023. [Online]. Available: https://assets.vlaanderen.be/image/upload/v1666582089/Visienota_Warmtep…;

[3] European Heat Pump Association (EHPA), ‘Heat Pumps in Europe - Key Facts & Figures’, no. May. Brussels, 2023. [Online]. Available: https://www.ehpa.org/wp-content/uploads/2023/06/Heat-Pump-Key-Facts-May…;

[4] European Heat Pump Association (EHPA), ‘European Heat Pump Market and Statistics Report 2023’, 2023. [Online]. Available: https://www.ehpa.org/news-and-resources/publications/european-heat-pump…;

[5] G. Reynders, T. Nuytten, and D. Saelens, ‘Potential of structural thermal mass for demand-side management in dwellings’, Build Environ, vol. 64, pp. 187–199, Jun. 2013, doi: 10.1016/J.BUILDENV.2013.03.010.

[6] A. Uytterhoeven, ‘Optimal Operation of Thermostatically Controlled Loads in Residential Buildings under Uncertainty From a Building to an Electricity System Perspective’, PhD thesis, KU Leuven, 2022. [Online]. Available: https://lirias.kuleuven.be/retrieve/653266

[7] D. Patteeuw et al., ‘CO2-abatement cost of residential heat pumps with active demand response: Demand- and supply-side effects’, Appl Energy, vol. 156, pp. 490–501, Oct. 2015, doi: 10.1016/j.apenergy.2015.07.038.

[8] C. Protopapadaki, ‘A probabilistic framework towards metamodeling the impact of residential heat pumps and PV on low-voltage grids’, Ph.D. thesis, KU Leuven, 2018. doi: 10.13140/RG.2.2.33034.72644.

Want to know more?

Are you interested in reading the full position paper which formed the basis of this Expert Talk?